Canceling a credit card involves terminating your account with the issuing bank, meaning you can no longer use that card for purchases or accumulate any further charges. While canceling a card may appear as a simple task, there are crucial nuances in understanding the impact of this decision, especially on your financial health and credit score. Individuals often overlook how canceling a credit card can affect their credit utilization ratio and overall credit history. In this guide, we'll explore the essential steps and considerations to take into account when thinking about canceling a credit card, providing you with comprehensive information to align your decision with your financial goals.

What Cancellation Entails

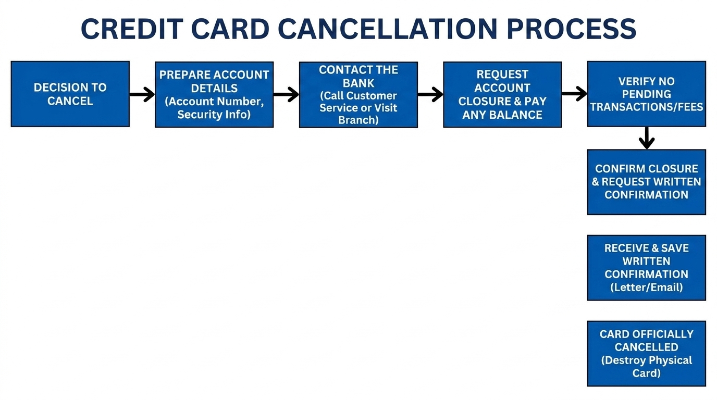

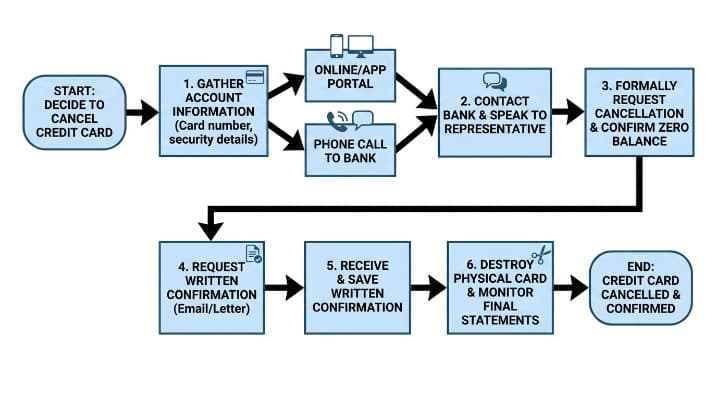

The process of canceling a credit card means closing the account associated with that card, eliminating the ability to use that line of credit for purchases. Once you decide to cancel, you will lose the credit limit attached to the card, which is a significant factor influencing your credit utilization ratio—a crucial element in determining your credit score. Thus, before moving forward with cancellation, it's important to weigh this decision carefully.

To initiate cancellation, it's typically advisable to contact your credit card issuer directly. Though you may manage your account online, speaking with a representative serves to confirm the cancellation process and clarify any questions you may have about outstanding balances or repercussions on your credit score. Ensure you also get a written confirmation of the cancellation to keep in your records. Following these steps can help you ensure that your cancellation process is well-handled and informed.

The decision to cancel a credit card may lead to several major implications for your financial standing. Chief among these is its potential impact on your credit score. Credit scoring models generally favor longer credit histories and a diverse array of open accounts. Canceling a credit card, particularly one with an extended history, can inadvertently reduce your average account age, which may in turn diminish your credit score. Additionally, if you maintain existing debt on other cards, ceasing to use one may spike your credit utilization ratio, further harming your credit profile.

Although it may seem prudent to close a credit card to prevent further spending, doing so can confine your financial agility in emergencies or hinder your journey toward achieving new financial objectives. Many mistakenly believe that having fewer credit cards is beneficial to their financial health, overlooking the advantages that can be accrued from keeping good credit habits alive and maintaining a higher available credit limit.

Moreover, there is a common misconception that canceling a credit card provides an immediate solution to existing debt difficulties. The reality is that such a decision often entails more complicated consequences. As a result, it's vital to contemplate the long-term repercussions on your credit health and overall financial stability before deciding to sever ties with a credit card. If you want to earn extra rewards from referrals, How to Get $50 for Every Successful Credit Card Referral explains a simple step-by-step method.

A Framework for Thoughtful Cancellation

When reflecting on whether to cancel a credit card, it's critical to assess several key elements to inform your decision-making. Start with a close examination of the annual fee attached to the card. If the fee outweighs the perks you enjoy—be it rewards, cash back, or travel benefits—then your decision to cancel could be justified. Next, review your usage patterns. Is the card being utilized enough to warrant its retention? A card that's used sparingly might not merit upkeep.

Consider the costs versus benefits. For instance, you may want to weigh the value of the rewards accrued against the annual fees charged. Earning $200 in rewards while paying $100 in annual fees presents a compelling reason to keep the card. However, if the costs surpass the benefits, it could signal the time for reevaluation.

Additionally, contemplate how canceling the card will influence your credit utilization ratio and average account age. To illustrate: imagine holding three credit cards with a cumulative limit of $10,000 alongside a balance of $2,000—resulting in a utilization ratio of 20%. If you were to cancel a card with a $2,500 limit, the calculation would alter your utilization to 25% ($2,000/$7,500), potentially inflicting damage on your credit score if other balances are maintained. Ultimately, it's important to carefully weigh these factors when deciding on the future of your credit card in relation to your financial circumstances.

Different Scenarios Influencing Credit Card Cancellation Decisions

When contemplating the cancellation of a credit card, various user types encounter distinct scenarios that greatly impact their decision pathways. Recognizing these perspectives can empower individuals to make informed choices.

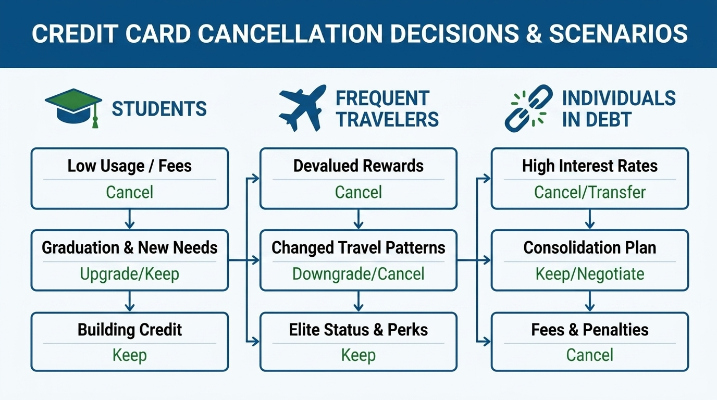

1. The Student

For many students navigating college, financial management poses a significant challenge. A student may contemplate canceling their credit card due to high-interest rates or the pressure of monthly payments. Yet, canceling too soon could detrimentally affect their credit score—an essential factor for securing future loans. In such cases, students may find keeping their card beneficial, particularly if they can maintain low balances and make timely payments that bolster their credit history.

2. The Frequent Traveler

Individuals who travel often rely on credit cards for their associated rewards and travel benefits. For this group, the continuation of a credit card may hinge on accumulating points for upgrades or eliminating foreign transaction fees. However, they should consider cancellation if their current travel card fails to deliver adequate returns. Evaluating retention against potential alternatives with better rewards can lead to more beneficial outcomes.

3. The Individual Struggling with Debt

For those experiencing financial uncertainty, canceling a credit card may seem like an appealing short-term relief from monthly expenditures. However, the ramifications of closing an account, such as negatively impacting credit scores and losing available credit, can have prolonged effects. Herein, a more tailored approach that evaluates interest rates and explores options like balance transfers could be prudent before making the final decision to cancel.

Through understanding the unique rationales of these user types, individuals are better equipped to navigate the intricacies of credit card cancellation.

Lessons from Real-Life Examples of Credit Card Cancellation

Consider the case of Jane, a 32-year-old marketing professional who chose to cancel her credit card after accruing substantial debt. Initially, Jane used her card for convenience, but her spending spiraled, resulting in overwhelming bills. By canceling her card, Jane anticipated a drop in her credit score. Nevertheless, she embraced this change as a necessary component of her financial recovery. Within a year of adopting a strict budgeting plan and refraining from new debt, Jane’s credit score rebounded and improved significantly. From her experience, she grasped the importance of financial discipline and how breaking free from credit reliance could ultimately restore her financial health.

On the flip side is Mark, a 45-year-old entrepreneur who canceled his credit card due largely to high annual fees that overshadowed any advantages. Although his immediate feeling was relief, he soon realized that he had lost out on important perks like cashback rewards and travel insurance that were integral during his numerous business trips. This taught Mark a valuable lesson about the need to carefully assess these trade-offs before canceling a card, leading him to prioritize examining terms and benefits in his future financial decisions.

These experiences underscore the necessity to think critically about canceling a credit card, revealing that while such decisions can initially feel burdensome, they can contribute to a more responsible financial journey when approached with careful thought and strategy.

Navigating Financial Futures

The decision to cancel a credit card is one that requires substantial contemplation. Throughout this article, we have emphasized the importance of assessing potential impacts on your credit score and your overall financial situation. Readers need to evaluate their unique circumstances and make decisions aligned with their financial aspirations. By utilizing the framework provided in this guide, you can handle the complexities of credit card cancellation with clarity and confidence. Ultimately, taking the time to consider the ramifications can pave the way for more favorable financial outcomes in the future.