Have you recently gone through the frustrating experience of having your credit card application rejected? For those accustomed to quick approvals, this unexpected denial can feel particularly jarring and even somewhat personal. But rest assured, you're not alone in this situation - application rejections happen to countless consumers for various legitimate reasons. The good news is there almost always a clear explanation behind the denial, and more importantly, actionable steps you can take to improve your chances for future applications.

Understanding the Most Frequent Reasons for Credit Card Application Denials

Qualifying for a credit card requires more than just completing an application form. Lenders carefully evaluate your financial profile, including your credit score, income level, and overall credit history. Even if you believe you meet all the requirements, your application might still be declined for several common reasons.

Incomplete or Inaccurate Application Information

One of the most preventable reasons for denial stems from improperly completed applications. Many applicants overlook crucial details like accurately reporting their income or employment information. Even with an impeccable credit history spanning decades, your application will be rejected if your reported income falls below the card minimum requirement. Always double-check that every field is filled out completely and accurately before submission.

Limited Credit History Despite Good Scores

It can be particularly frustrating when you maintain an excellent credit score but still face rejection due to what lenders perceive as an insufficient credit history. This situation typically means you need more time to establish a longer track record of responsible credit use before qualifying for certain premium cards. Consider building your history with starter cards before reapplying.

High Credit Utilization Ratios

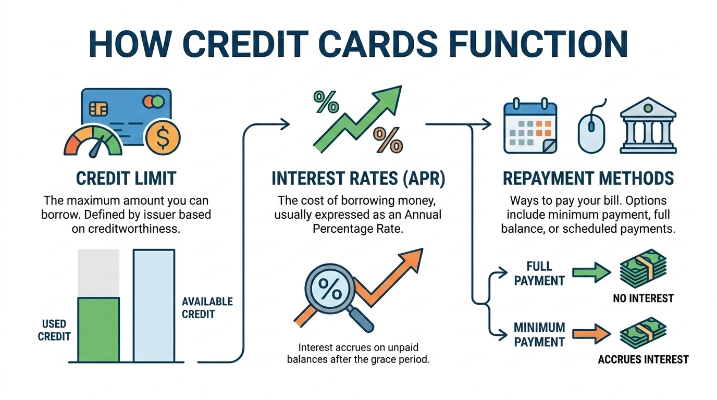

Lenders prefer to see applicants using only a portion of their available credit. Ideally, you should keep your credit utilization below 30% across all cards. If you're consistently maxing out your current cards or carrying high monthly balances, creditors will view you as a higher risk. Paying down existing balances before applying can significantly improve your approval odds.

Recent Negative Marks on Your Credit Report

Recent collections accounts, legal judgments, or other negative public records can immediately impact your creditworthiness. While these items lose their sting over time (typically remaining for 7-10 years), recent negative marks can be particularly damaging to your approval chances. If this applies to you, focus on resolving any outstanding issues before reapplying.

Excessive Recent Credit Inquiries

Each credit card application triggers a hard inquiry on your credit report. Multiple applications in a short period can signal financial distress to lenders. There no universal limit, but spacing out applications by at least six months demonstrates more responsible credit-seeking behavior.

Strategic Steps to Take After a Denial

Rather than wasting energy arguing with customer service representatives, take these constructive steps to improve your future approval chances.

Carefully Review Your Adverse Action Notice

By law, creditors must provide a written explanation (called an Adverse Action Notice) within 7-10 business days of denial. This document outlines the specific reasons for rejection and serves as your roadmap for improvement. Pay close attention to the cited reasons, as they'll guide your next steps.

Obtain and Scrutinize Your Credit Reports

You're entitled to a free copy of your credit report after a denial. Obtain reports from all three major bureaus and review them meticulously for errors. Dispute any inaccuracies immediately, as correcting mistakes can quickly improve your credit standing.

Analyze Your Credit Score

Along with your credit reports, you should receive your current credit score. Compare this against the lender requirements and identify areas needing improvement. Common focus areas include payment history, credit utilization, and length of credit history.

Develop a Targeted Credit Improvement Plan

Based on your review, create a customized plan to address your specific credit weaknesses. This might involve paying down balances, limiting new applications, or addressing any delinquent accounts. Set measurable goals and timelines for improvement.

Consider Alternative Credit Products

If traditional cards remain out of reach, explore secured credit cards or retail store cards with more lenient approval standards. These can help rebuild your credit when used responsibly. Just be mindful of potentially higher interest rates or fees associated with these products.

Utilize Pre-Approval Tools

Before your next application, take advantage of online pre-approval tools that perform soft inquiries (which don't affect your credit score). These provide valuable insight into your approval odds without the risk of another hard inquiry.

Final Thoughts

While a credit card denial can feel discouraging, it often just a temporary setback. By understanding the reasons behind the rejection and taking deliberate steps to improve your financial profile, you can significantly enhance your chances of approval in the future. Remember that building and maintaining good credit is a marathon, not a sprint - patience and consistent responsible behavior will ultimately lead to success in your credit journey.