Credit cards are essential financial tools that provide consumers with the ability to efficiently manage credit. At their core, credit cards allow individuals to borrow funds from a lender—typically a bank—for purchases of goods and services, up to a predefined limit. This system not only grants immediate access to capital but also aids in building a credit history, which can facilitate future loan approvals and other financial opportunities. Understanding the nuances of how credit cards function can empower users to make informed financial decisions, ultimately leading to smarter spending and optimal saving habits. For a broader financial reset, 7 Actionable Ways to Skyrocket Your Financial Standing breaks down key actionable steps.

How Credit Cards Work

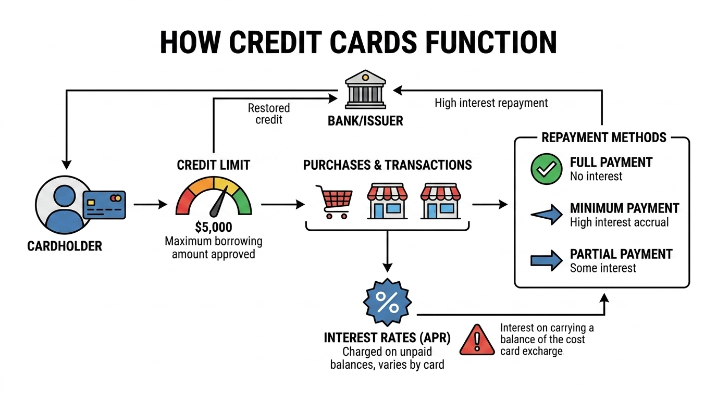

Credit cards function as a convenient way to borrow money up to an agreed-upon credit limit. When a purchase is made using a credit card, you are effectively taking out a short-term loan from the card issuer, which requires repayment. This borrowing incurs a cost, represented by the Annual Percentage Rate (APR), the yearly interest rate you are charged on any outstanding balance. It's crucial to note that if the balance is not paid in full by the due date, interest accrues based on the APR.

Each billing cycle, a minimum payment is required, which is the smallest amount you can pay to avoid penalties. This is often a small fraction of the total owed or a fixed dollar amount.

By using credit cards responsibly, individuals can reap numerous benefits, including building a positive credit history, earning rewards or cash back, and providing a financial cushion for unexpected costs. To lead a balanced financial life, it’s critical to pay off the full balance each month, adhere to a budget, and avoid falling into the trap of relying on credit for regular expenses. Practicing these habits ensures that you enjoy the advantages of credit cards while keeping debt manageable and your credit score strong.

The Significance of Credit Cards in Modern Finance

Credit cards have become integral to modern financial management, serving not only as instruments for making purchases but also as effective tools for enhancing financial wellbeing. One of the primary functions of credit cards is their contribution to establishing a credit history and credit scores. Credit history reflects an individual's capability to repay debt, while a credit score—a numeric expression of that history—ranges from 300 to 850. Lenders utilize these scores to assess creditworthiness, which influences loan approvals and the associated interest rates.

Additionally, many credit cards incorporate reward systems, such as cash back or points, to stimulate wise spending. For example, a consumer might earn 1.5% cash back on every purchase, encouraging thoughtful purchases while simultaneously benefiting financially from their transactions. Point accrual systems also enable users to collect credits toward travel or other rewards, adding extra value to everyday shopping experiences and promoting exploration and enjoyment.

Moreover, the convenience provided by credit cards can significantly affect consumer spending behaviors. While they facilitate easier financial transactions, there is a risk of excessive spending that can lead to detrimental financial habits. When wielded wisely, however, credit cards can encourage accountability in tracking expenses, timely bill payments, and maintaining balanced debt levels, ultimately fostering better overall financial health. Therefore, diligent management of credit cards can yield a range of benefits while also necessitating a responsible approach to debt.

Understanding Interest on Outstanding Balances and Effective Debt Management

Grasping how interest is calculated on outstanding credit card balances is essential for responsible debt management. The interest charges can be calculated using the following formula: Interest = (Outstanding Balance * APR) / 365 days * Number of days outstanding.

Here’s a breakdown of each component:

- Outstanding Balance: This refers to the amount owed on your credit card.

- APR: This is the Annual Percentage Rate, representing the interest rate applied to the borrowed amount annually.

- Daily Interest: To find the daily interest rate, divide the APR by 365.

- Days Outstanding: This is simply the number of days the balance remains unpaid.

For instance, if you hold a balance of $1,000 with an 18% APR, and you do not pay it down for 30 days, the interest calculation would be as follows:

- Daily Interest = (0.18 / 365) = 0.000493

- Interest = ($1,000 * 0.000493) * 30 = $14.79.

Most credit cards also offer grace periods, generally lasting between 20 and 30 days post-billing cycle, during which you can pay your balance without incurring any interest. To avoid these charges, aim to consistently settle your total balance within this timeframe.

Implementing effective strategies to manage credit card debt can significantly enhance financial control. Here are a few actionable tips:

- Pay More Than the Minimum: Prioritize paying more than the minimum amount due to accelerate balance reduction.

- Create a Budget: Keep an accurate record of your expenditures while allocating funds specifically for credit card payments.

- Utilize Automatic Payments: Set notifications or automate payments to ensure bills are paid on time.

- Monitor Spending Habits: Steer clear of unnecessary purchases on your credit card to maintain a sustainable balance.

- Consider Debt Consolidation: If your debt feels overwhelming, investigate consolidation loans or seek financial assistance.

By acquiring a solid understanding of interest calculations and adopting effective management for credit card debt, you can gain control over financial obligations, reduce unnecessary expenses, and boost your overall financial well-being. How to Get $50 for Every Successful Credit Card Referral explains how to turn referrals into consistent rewards.

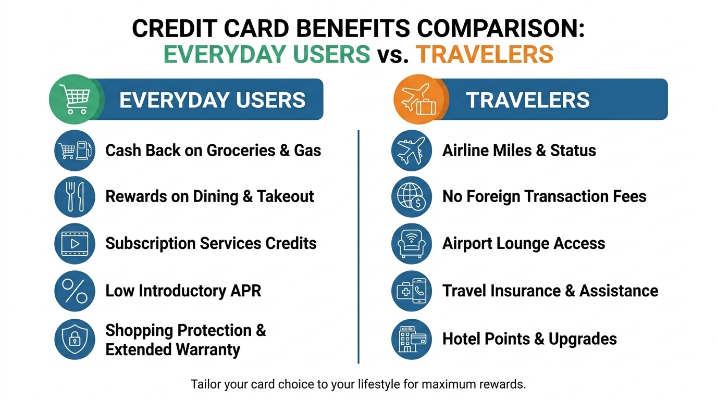

Different User Types in Credit Card Usage

In the realm of credit cards, the user experience greatly varies, reflecting a spectrum of habits and needs. Everyday users often depend on credit cards for routine purchases and bill payments, weaving them seamlessly into their budgeting practices. For instance, a college student may utilize a credit card for groceries and subscription services, reaping the benefits of points and cash back. However, this spending could easily grow unchecked, resulting in debt and significant interest repayments if not tracked appropriately.

Conversely, travelers leverage credit cards for exclusive perks such as travel rewards and associated insurance. A frequent flyer might use a specialized rewards credit card to accumulate points for free flights or hotel stays. Nonetheless, if this traveler exceeds their budget in pursuit of enticing travel deals, they risk significant financial pitfalls.

These distinct scenarios underscored the importance of maintaining balance: credit cards possess the potential to offer considerable advantages, but they also demand prudent management to circumvent the dangers of overspending and poor fiscal choices. By considering both positive opportunities and cautionary tales, consumers can navigate the credit card landscape with greater wisdom and effectiveness.

Everyday Scenarios Illustrating Credit Card Benefits

In the bustling aisles of a grocery store, we find Sarah, an everyday shopper maximizing the advantages of her credit card’s cash back rewards. As she collects her essentials, Sarah is acutely aware that every dollar spent serves to earn her cashback, accumulating into substantial returns at the end of each quarter. This beneficial strategy allows her to save on future grocery expenses, turning her routine spending into an avenue for savings.

Across the world in London, we meet Mark, a frequent traveler capitalizing on a credit card specifically designed for international use. With zero foreign transaction fees and rich travel benefits, he books flights and accommodations abroad without the anxiety of unexpected costs. Every transaction abroad not only earns him travel points but also opens doors to exclusive airport lounges, transforming his travels into rewarding adventures.

Harnessing the Power of Credit Cards for Financial Strength

To comprehend the complex mechanisms that govern credit cards is vital for anyone aspiring toward financial health. This piece has explored critical elements such as the workings of credit cards, their myriad benefits, and their day-to-day applications. Establishing responsible use practices such as punctual payments and diligent spending saves individuals from falling into debt and helps maximize rewards.

Ultimately, a thorough understanding of credit card functionality enhances consumer knowledge, empowering informed decision-making that fosters financial resilience while leveraging the myriad benefits these powerful financial instruments provide.