The Annual Percentage Rate (APR) is a fundamental concept for anyone engaged with credit cards. It reflects the total cost of borrowing, integrating both the interest rate and additional fees, making it an essential element in financial decision-making. Grasping what constitutes a competitive APR can markedly influence your spending behavior and overall financial well-being, as it can lead to substantial savings over time. This article delves into the characteristics of a good APR, examining typical rates, factors affecting these percentages, and their impacts on consumers based on varying credit profiles. By the end, readers will possess a thorough understanding of the significance of APR and practical guidance for selecting the best credit card suited to their needs. For beginners, 4 Practical Steps for a $300 Credit Card Signup Reward shows how to earn introductory credit card rewards.

What Constitutes a Good APR for Credit Cards?

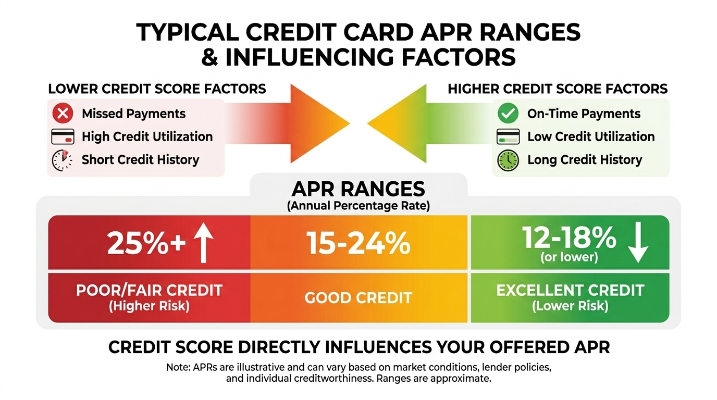

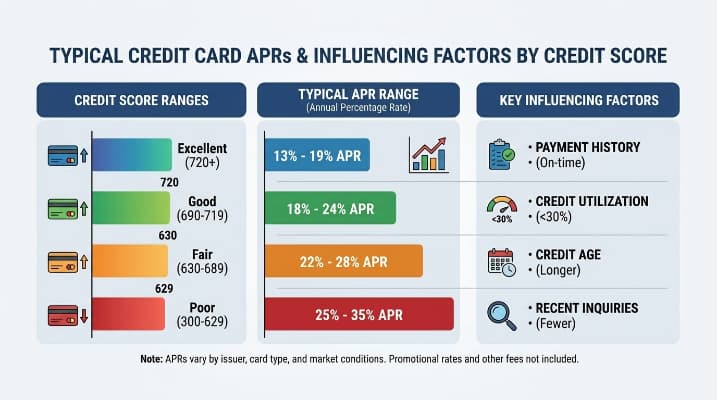

Generally, a favorable Annual Percentage Rate (APR) for credit cards ranges from 14% to 24%. These rates can vary significantly depending on an individual's credit score. Borrowers with excellent credit histories often qualify for lower APRs, while those with poor credit ratings may be subject to much higher rates. For instance, as reported by the Federal Reserve in 2023, the national average interest rate on credit cards stands at approximately 19.49%.

It is important to understand that credit cards designed for rewards or additional perks frequently have APRs surpassing 24%. Conversely, cards offered to consumers with limited or no credit history often begin at rates of 25% or higher. Hence, individuals boasting a credit score typically above 700 should strive for APRs on the lower end of the spectrum, ideally around 15% or even less for premium options. Those with credit scores in the poor or fair range (below 650), however, should approach high APRs cautiously, as rates nearing 25% may become commonplace.

Ultimately, actively comparing various offers is essential to secure an optimal APR that aligns with your credit profile—especially as even a marginal difference in rates can culminate in significant long-term savings. If you want to take advantage of bank offers, 4 Practical Steps to Get a $250 Bonus from Bank Promotions explains how to qualify for promotional rewards.

The Importance of APR and Its Effects on Consumers

The APR is vital for credit card users as it directly affects the costs associated with carrying a balance. The yearly interest on outstanding credit represented by the APR can have substantial implications for consumers. Higher APRs can cause a drastic increase in total amounts owed, especially for those who prefer not to pay their balances in full each month. For example, carrying a $1,000 balance on a card with an 18% APR can accrue approximately $180 in interest over a year, emphasizing how costly high rates can be.

In contrast, a lower APR, such as 10%, would incur only $100 in interest on the same balance, resulting in $80 in savings annually. This dynamic illustrates the necessity for consumers to shop wisely for credit cards with competitive rates, as even slight shifts can yield notable financial benefits.

Moreover, understanding APR paves the way for effective financial strategies. Users with high APRs may choose to prioritize balance repayment to prevent burgeoning debt, while those with lower APRs can afford to carry a balance with greater ease, providing potential financial flexibility.

Responsible credit management is critical in this scenario; striving to pay off balances consistently, avoiding credit limit max-outs, and preventing unnecessary debt accumulation are essential steps. In addition, a long-term financial outlook necessitates factoring in APR when selecting cards, as choosing those with advantageous rates can foster better credit health, alleviate financial stress, and enhance overall financial security.

Calculating Interest Costs Using APR

To understand how APR influences interest payments, consider the following guideline for calculating interest costs:

Interest = (Principal × APR × Time) / 100

Where:

- Principal is the amount borrowed or the credit card balance

- APR is the annual interest rate expressed as a percentage

- Time is the duration of the loan in years

Hypothetical Example for Monthly Payments

Imagine a scenario where you possess a credit card balance of $1,000 with an APR of 18%. The steps to calculate your monthly interest cost involve first determining the annual interest:

- Interest = (1000 × 18 × 1) / 100 = $180 (for annual interest)

- Dividing this figure by 12 yields the monthly interest cost: $180 / 12 = $15

Thus, each month, a $15 interest charge would be added to your outstanding balance should no payments be made.

Factors Impacting APR

Numerous elements can influence the APR offered by credit card companies:

- Credit Utilization: Maintaining low credit balances relative to total available credit can help secure a more favorable APR; a higher utilization ratio can denote increased risk for lenders.

- Payment History: A track record of prompt payments signals dependability, potentially lowering your APR. Conversely, late payments can lead to elevated interest rates.

Comprehending these key factors is essential for efficient credit management and minimizing interest costs. By adopting informed practices, consumers can greatly alleviate their financial burdens.

Diverse User Scenarios and Their Interaction with APR

Exploring different user scenarios illuminates how varying credit profiles perceive APR and the unique challenges they face.

1. Users with Excellent Credit:

Individuals with exceptional credit scores (typically 750 and above) frequently access the best APR offers. They tend to consider APR a formality due to their low rates, focusing instead on reward maximization. Nonetheless, the danger of overspending could lead to debt issues. To handle APR adeptly, these users must prioritize clearing their balances monthly, taking advantage of promotional deals without succumbing to debt pitfalls.

2. Users with Poor Credit:

Conversely, individuals grappling with poor credit (below 600) often burden themselves with drastically higher APRs. For them, APR represents a significant obstacle as exorbitant interest tends to further complicate their financial lives. These users may feel entrapped by debt, struggling to manage minimum payments. Strategies to combat these challenges include focusing on credit-building habits such as timely bill payments, utilizing cards tailored for rebuilding credit, and keeping low balances to avoid excessive interest charges.

Both these scenarios highlight how understanding one's credit position is essential for customizing approaches to managing APR, ultimately leading to improved financial well-being.

Navigating Real-life APR Challenges

Consider Maria, a recent college graduate who obtained her first credit card with a steep 24% APR. Enthusiastic at first, she soon realized that carrying a balance came with considerable interest fees. A few months of only making minimal payments escalated her debt, prompting her to rethink her spending. A pivotal lesson for Maria was the importance of paying off her balance entirely to sidestep high interest.

In contrast, John's experience illustrates the benefits of securing a lower APR. He acquired a rewards credit card at 15% APR. By adhering to a disciplined budget and ensuring he paid off his total balance monthly, John enjoyed not just points for travel opportunities, but also substantial savings compared to Maria's situation. His journey underscored the significance of shopping for better APR options and how doing so positively influenced his finances.

These real-world cases emphasize the necessity of comprehending APR. Awareness of the varying impacts of different rates on financial strategies can guide consumers like Maria and John to make more beneficial financial decisions and outcomes.

Empower Yourself with Knowledge on APR

Recognizing the importance of APR is essential for every credit card user, as it profoundly impacts your financial status. By understanding the critical nature of selecting an appropriate APR, you are equipped to make informed credit card choices. Assessing your credit circumstances can reveal valuable opportunities for savings and optimal credit management practices. Selecting credit cards with advantageous APRs can amplify your purchasing power while minimizing interest costs over time. Seize the opportunity today—evaluate your credit options and make thoughtful choices to ensure a better financial future.