An emergency fund serves as a financial safety net during crises, safeguarding your savings from unexpected expenses like medical bills, car repairs, or sudden job loss. Determining how much emergency fund you really need is vital for achieving financial stability and peace of mind. This article seeks to provide direct answers and actionable guidelines to help you ascertain the ideal amount required for your situation. By establishing a robust emergency fund, you can enhance your financial security and significantly mitigate the stress that accompanies unforeseen financial challenges. You can explore 7 Actionable Ways to Skyrocket Your Financial Standing for actionable steps to strengthen your finances.

Defining an Emergency Fund

An emergency fund is defined as a dedicated savings account designated for unplanned expenses or emergencies. It functions as a financial buffer that empowers you to handle unexpected costs, such as healthcare bills, vehicle repairs, or income loss, without resorting to debt.

When considering how much to save in this fund, a common recommendation is to have three to six months’ worth of living expenses readily available. This range aids you in managing unforeseen circumstances comfortably. Factors like job security and family obligations can heavily influence the sum required. For instance, if you hold a stable position, you might only need three months' worth of expenses. However, for those employed in fluctuating industries or with dependents relying on them, it’s wise to aim for a larger financial cushion of six months or even more.

Additionally, you should assess your fixed monthly expenses, such as rent, utilities, and food, alongside your overall income stability. For example, someone with a steady paycheck might prioritize a smaller emergency fund compared to a freelancer whose earnings can vary widely.

In summary, a thorough evaluation of your personal situation is necessary to establish an emergency fund that offers both security and peace of mind.

The Essential Nature of an Emergency Fund

An emergency fund is a cornerstone of financial well-being, ensuring protection against life’s unpredictability. In the absence of sufficient savings, individuals risk spiraling into debt during challenging times—consider the sudden car repairs or unexpected medical bills that could easily jeopardize financial stability. Imagine receiving unexpected news of job loss; without an emergency fund, you may be compelled to depend on high-interest credit options to stay afloat, potentially leading to an inescapable cycle of debt.

Emergencies often occur when least anticipated, catapulting individuals into financial distress. Unexpected medical expenses can arise rapidly from accidents or health issues, and the subsequent bills can accumulate swiftly, forcing you to scramble for resources. Moreover, the anxiety associated with not having readily available funds to address these issues can take a toll not just on your financial condition but also on your mental health, impacting your overall quality of life. Sufficient savings equate to peace of mind, allowing you to navigate life’s complexities without the added burden of financial uncertainty. By setting aside an emergency fund, you’re not merely preparing for the unpredictable—you’re investing in your tranquility and securing a more stable financial future.

Calculating Your Emergency Fund

Creating a financial safety net via an emergency fund is essential for managing life’s uncertainties. The following framework will assist you in determining the ideal amount necessary for your emergency fund via a simple three-step formula.

- Assess Monthly Expenses

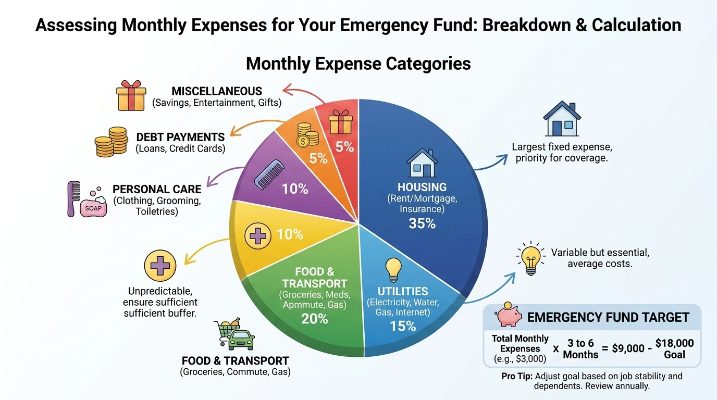

Begin by compiling your monthly expenses. Create a comprehensive list that identifies both essential fixed costs (including rent or mortgage, utilities, and insurance) and variable costs (like groceries, transportation, and personal care). For practical purposes, let’s assume your total monthly expenses amount to $3,000. - Evaluate Personal Risk Factors

Next, analyze your unique factors. Consider elements such as job stability (Are you secure in your role, or is your position susceptible to layoffs?), health risks (Are you prone to regular medical issues?), and the number of dependents (Are there children or other family members depending on you?). Increased risk rates may necessitate a larger financial cushion. Assuming you determine a requirement for five months of cushion due to a less stable job and caring for two dependents, you’ll want to factor that in. - Calculate Total Emergency Fund Needed

To find your total emergency fund necessary, multiply your monthly expenses by the number of months you identified as prudent. In our example, this would be:

Total Emergency Fund = Monthly Expenses × Recommended Months of Cushion

Total Emergency Fund = $3,000 × 5= $15,000

Thus, based on your analysis, aiming for an emergency fund of $15,000 provides you with financial security and peace of mind as you confront unforeseen events. It is essential to periodically revisit your calculations, particularly if your financial situation evolves.

Tailoring Emergency Fund Needs to Individual Scenarios

In our increasingly unpredictable economic environment, grasping the specific needs of different user profiles is essential for accurately determining an emergency fund amount. Here, we focus on three distinct groups and their unique requirements.

1. Young Professionals with Limited Obligations

Young professionals starting in their careers typically have fewer financial responsibilities. Their emergency fund benchmarks may be minimal, focusing on covering essentials like rent and student loans. With limited family obligations, the recommended savings are usually three to six months’ worth of essential expenses. Nevertheless, as job markets can fluctuate, slight additional padding can promote peace of mind during transitional phases or unexpected job losses.

2. Families with Dependents

Families encounter different challenges requiring careful consideration in emergency fund calculations. With dependents depending on them, parents must account for both personal costs and those related to their children—such as childcare and education expenses. A recommended approach for families is targeting six to twelve months’ worth of expenses within their emergency fund. This extended buffer safeguards against unemployment, medical emergencies, or other unexpected financial challenges, ensuring that dependents can maintain their quality of life.

3. Self-Employed Individuals

Self-employed individuals frequently face variable income flows and lack employer-funded benefits. As a result, they often require a more substantial emergency fund due to increased financial volatility, which can lead to heightened stress during lean periods. For these individuals, it is advisable to save six to twelve months' worth of expenses to provide adequate support during fluctuating income phases and cover business liabilities without adversely affecting their personal finances.

Recognizing these differing scenarios emphasizes that there is no blanket solution regarding emergency funds. Tailoring the fund to align with specific individual circumstances provides a clearer pathway to establishing financial security.

Lessons from Real-Life Emergency Fund Experiences

Consider Jessica and Mark, a young couple who faced sudden job loss when Mark was laid off as a result of company downsizing. Fortunately, they had diligently saved an emergency fund equivalent to six months’ worth of living expenses. This financial cushion enabled them to manage their rent, utilities, and daily necessities without accruing debt. Jessica landed a new job within two months, allowing them to emerge from this setback with their finances largely intact, solidifying their commitment to ongoing savings.

Conversely, we have James, who neglected to prioritize establishing an emergency fund. Following an abrupt medical emergency requiring a hospital visit, James found himself ill-equipped and had to rely on credit cards for his bills. The debt accumulated rapidly, placing him in a precarious financial situation marked by mounting high interest.

These instances underline a fundamental lesson: maintaining an emergency fund not only fosters security and assurance in the face of unexpected events but also serves as a deterrent to financial troubles when such emergencies arise. Allocating funds for emergencies isn't simply a precaution—it represents an essential aspect of responsible financial planning.

Take Control of Your Financial Future

In summary, an emergency fund is an indispensable aspect of financial resilience that acts as a buffer during unforeseen circumstances. Throughout this guide, we’ve explored critical factors to consider when determining the required amount for your emergency fund, including personal expenses, income stability, and lifestyle transitions. Establishing this safety net not only diminishes the anxiety associated with unplanned expenses but also empowers you to make informed financial decisions. Now that you comprehend its significance, take actionable steps to evaluate your financial needs and begin calculating your emergency fund today. Remember, the sooner you start, the more robust your financial security can be for the future