Credit cards are financial instruments that enable individuals to make purchases by borrowing funds, which are repaid at a later date, typically with added interest. Recognizing the importance of how many credit cards to possess is vital for sound financial planning. The ideal number can enhance one’s credit score, afford financial flexibility, and enable strategic spending. Conversely, having too many or too few credit cards can complicate financial management and decision-making. This article explores the ideal number of credit cards tailored to individual financial situations and goals, paving the way for thoughtful management and informed decision-making. If you want to make the most of credit card bonuses, 4 Practical Steps for a $300 Credit Card Signup Reward explains a simple step-by-step approach.

Recommended Number of Credit Cards

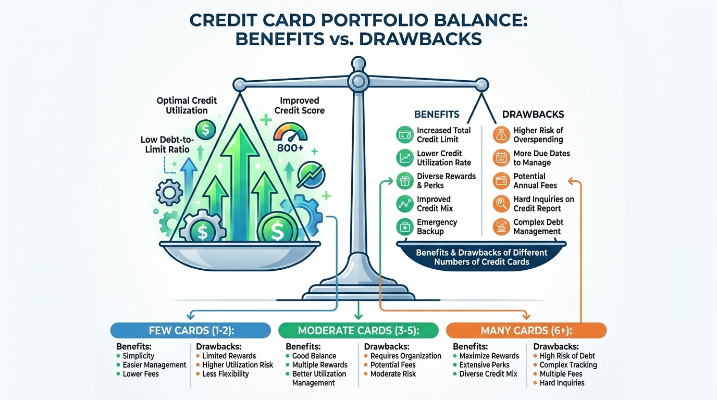

When contemplating how many credit cards to own, experts generally recommend maintaining between one and three. This flexibility allows individuals to customize their credit card holdings to suit their specific financial situations and credit management styles. A single credit card can simplify management, making it easier to track spending. Meanwhile, holding three can enhance one’s credit utilization and available credit, provided it does not lead to overwhelming debt.

Striking a balance that aligns with your financial needs is essential; this enables effective expense management while maximizing rewards and benefits. Furthermore, a low credit utilization ratio—achieved by distributing expenses across multiple cards—can favorably influence your credit score. Thus, the optimal number of credit cards is subjective, reflecting personal preferences and financial aspirations, all while ensuring manageable debt and effective credit management practices remain front and center.

The Importance of Credit Card Management

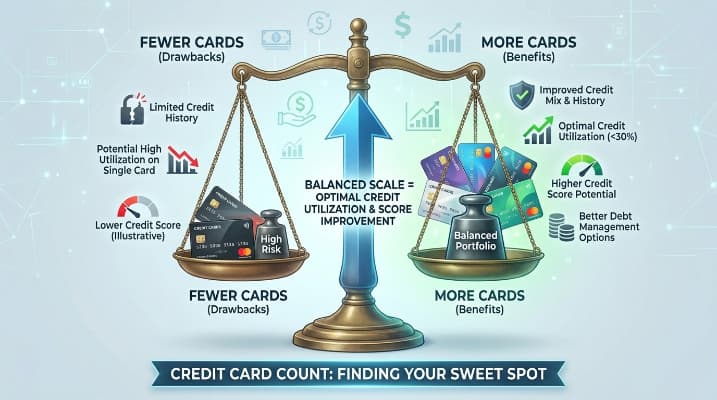

Managing the quantity of credit cards in one's possession is crucial for preserving a healthy credit profile. A key concept to understand is credit utilization, which measures the ratio of credit used to total available credit. Generally, a lower credit utilization ratio—ideally below 30%—contributes to a better credit score. For example, if an individual has a credit limit of $10,000 across five cards but only charges $2,000, their utilization stands at 20%. In contrast, having fewer cards with the same limit, yet charging $3,000, can severely damage one’s credit score due to higher utilization.

Furthermore, establishing a strong credit history is indispensable. Credit scores are shaped not only by credit utilization but also by the length of your credit history. A longer credit history reflects the borrower’s ability to manage credit responsibly. For instance, maintaining a couple of older accounts—even with minimal activity—can enhance one’s credit score relative to having an abundance of newer accounts, which might suggest financial instability.

Additionally, accumulating too many cards might result in missed payments and escalating debt, both of which adversely affect credit scores. Therefore, sustaining a manageable number of credit cards is essential for optimizing credit scores and fostering a positive financial future without incurring unnecessary risks. How to Get $50 for Every Successful Credit Card Referral explains how to turn referrals into consistent rewards.

A Framework for Assessing Your Credit Card Needs

To determine the optimal number of credit cards, it's imperative to scrutinize financial goals, spending habits, and preferences for rewards. This structured framework offers guidance for aligning your credit card ownership with your personal financial situation.

1. Financial Goals:

Start by identifying your primary objective. Is it paying off existing debt or establishing your credit score? If you are focused on debt repayment, one credit card with a low-interest rate may suffice to streamline your payments. However, if building credit is your priority, diversifying your cards can be beneficial, as long as you keep utilization low and consistently pay off your bills on time.

2. Spending Habits:

Evaluate your spending patterns. For frequent high-value purchases, holding several credit cards can be advantageous to maximize rewards and additional benefits. High spenders may leverage various cards to optimize cashback or points systems that align with their purchase categories (e.g., travel or groceries). Conversely, if your spending is relatively limited, a few well-selected cards may adequately meet your requirements without incurring numerous fees.

3. Rewards Tiers:

Lastly, assess the optimization of the rewards programs related to potential cards. Different cards provide different reward structures—some may benefit travelers, while others cater to everyday cashback opportunities. By understanding which rewards correlate with your purchasing habits, you can strategically select cards that enhance your overall financial benefits.

By scrutinizing these factors, you can better align your credit card strategy with your financial objectives and individual priorities in financial management.

Diverse User Scenarios in Credit Card Management

Credit card management strategies vary significantly among different user types, influenced by their financial situations and objectives.

Young Adults:

For many young adults starting their credit journey, a key focus is often on building a positive credit history while managing student loans and everyday expenses such as rent and groceries. Typically, they may opt to hold one or two credit cards—often including a low-limit student card alongside a secured card. This approach allows them to earn rewards on their spending while ensuring timely payments, which can lead to a substantial improvement in their credit score over time.

Families:

Families, managing diverse expenses such as mortgages, children’s education, and vacations, frequently find a need for multiple credit cards. For example, they might allocate one card for groceries that offers cash back, another to maximize travel rewards, and a third for larger purchases during promotional periods with no interest. This carefully calculated strategy not only allows them to optimize rewards but also facilitates a manageable payment schedule amid fluctuating expenses.

Business Owners:

Business owners often utilize credit cards as financial tools for investment in their companies. Many possess several cards to keep business and personal expenditures distinct, streamline cash flow, and take advantage of various business credit offers. For instance, a small business owner may leverage a card that offers travel benefits for client meetings, along with another providing rewards for office supply expenditures.

In essence, the number of credit cards maintained can vary considerably based on individual circumstances and financial aspirations. A solid understanding of what is needed can lead to optimized credit card usage, establishing a sturdy credit foundation.

Practical Insights

Case Study 1: Young Adult

Jessica, a 24-year-old recent college graduate, successfully opened her first credit card to cultivate her credit history. She consistently pays off her full statement each month, thereby maintaining a low credit utilization ratio and high credit score. Six months later, thanks to her responsible management, she received a credit limit increase, further enhancing her credit profile. As a result, she secured a loan for her first vehicle, paving the way for greater financial independence. Jessica’s diligent efforts contributed not only to her improved credit score but also to her preparation for future financial needs.

Case Study 2: Rewards-Minded Family

The Garcias, a family of four, have skillfully managed three credit cards to optimize rewards. They utilize one card exclusively for groceries, a second card for travel expenses, and a third for general purchases. By paying off their monthly balances fully, they avoid unnecessary interest while efficiently accumulating cashback and points. This method has enabled them to amass enough rewards to fund a family vacation without incurring additional costs. Their disciplined approach has not only provided significant travel benefits but also maintained a favorable credit utilization ratio, positively impacting their credit scores.

Case Study 3: The Strategic Business Owner

Mark, a small business owner, effectively uses four credit accounts for distinct purposes: one for business expenses, another reserved for emergencies, a third aimed at promotional efforts, and a fourth designated for rewards on office supplies. By strategically utilizing various accounts, Mark gains crucial insights into his spending habits, aiding in budgeting and financial forecasting. He diligently monitors payment deadlines to avoid any late fees, thereby preserving his business credit score. This layered approach allows him to leverage rewards while ensuring his financial health remains robust.

These case studies exemplify how tailored credit card strategies can distinctly influence personal financial well-being and credit health.

Tailored Strategies for Credit Card Management

Effectively managing credit cards revolves around achieving a careful balance tailored to individual circumstances. Throughout this exploration, we have reviewed how the ideal number of credit cards is contingent upon personal financial situations, goals, and management practices. You need to reflect on their financial habits and the broader impacts of credit card usage on their overall economic welfare. By making deliberate choices surrounding credit card ownership, individuals can maximize their credit’s potential while minimizing associated debt risks.